Tune in to our podcast series: The Dental Board Room

Listen Now

In this episode of The Dental Boardroom Podcast, Wes Read, CPA, CFP, continues the series on turning financial chaos into financial freedom for dental practice owners. Building on previous episodes covering team assembly, personal financial planning, and implementation strategies, Wes dives deep into the third step: developing a business financial plan that supports your personal financial goals.

He explains why organizing your financial reporting is the foundation for success, how to interpret monthly financial “X-rays” of your practice, and why understanding your break-even points is critical for long-term wealth accumulation.

Whether you’re aiming to stabilize cash flow or strategically grow your practice, this episode offers the insights you need to take the next step toward financial clarity and independence

Visual Reference: Break-Evens Chart

Transcript:

Wes Read: [00:00:00] Welcome everybody to another episode of the Dental Boardroom podcast. It's Wes Reed, C-P-A-C-F-P, coming at you carrying on my series on financial planning for dental practice owners turning financial chaos into financial freedom. Up to this point in my recent episodes, we covered the first few steps in the process of good dental financial planning.

Those steps were, number one, assemble your team and create a cadence for how often you meet with that team. Part two is develop a personal financial plan for financial independence. How do you attach meaning to your money? Number three is how do you create a business financial plan that supports your personal financial plan?

And then lastly, number four, implement, monitor, and revise. So today we are on that third segment of this journey of dental financial planning. It is organizing, it is [00:01:00] Europe, uh, developing a business financial plan. Now, the first step in developing a business financial plan was organizing your financial reporting.

These are your financial statements, your balance sheet, your financial forecast. It's really getting those numbers every month to tell you a story about the health of your practice. In the prior month, year to date, and changes from prior year to date to start seeing trends, you're a client. At Practice CFO, we dish out every month an additional report called the CFO Analysis.

The CFO analysis takes a much deeper dive through sort of trend data, graphical views to compare how you're doing against the goals that we've established together. And how are you doing against your peers in the industry? And as you know, the last report or page on that monthly CFO analysis that we send is, where did my cash go?

It's a really valuable report because over the years, [00:02:00] many times I've had many dentists say, Wes, I worked really hard. I had great collections, but honestly I don't know where my money went. So that report is a great one to help you answer that question. So let's carry on with step two in business financial planning.

Again, step one was, was organizing or creating a process of having good financial statements delivered every single month as a visual financial x-ray to understand the economic health of your dental practice. So now that you have that going to these sort of monthly x-rays, financially speaking, now let's go into a little bit more complicated topic, but one that I think provides incredible value, valuable insight to dentists to understand some key financial aspects of what it means to own a dental practice.

Now I wanna emphasize something about this point. This step and [00:03:00] this step is understanding your breakevens. You've heard of breakevens from maybe a practice management software. Maybe they call it your bam. What do you need to collect? Or what is your target collections every month in order to meet certain financial obligations.

Now, wealth accumulation does not start until you have satisfied key breakevens. How much do you need to collect to cover the various obligations? In your business checking account, and it's not until after all these obligations are met, your debt is taken care of, your taxes are taken care of, and paying yourself today is taken care of.

It's only after all of that break even do you start to pierce the financial independence break even. Do you start to actually fund. Uh, your personal balance sheet, which will then take care of you later as you rely on your personal balance sheet. IE interest dividends, capital gains, and other forms of income to take care of [00:04:00] you when you're no longer working for money.

So let's go through these breakevens because as I do this, I hope it gives you a keener insight into the inflection points throughout the month when your collections are coming in, at which time you sort of check off certain, uh, financial boxes, or you meet certain breakeven elements of your journey toward funding financial independence.

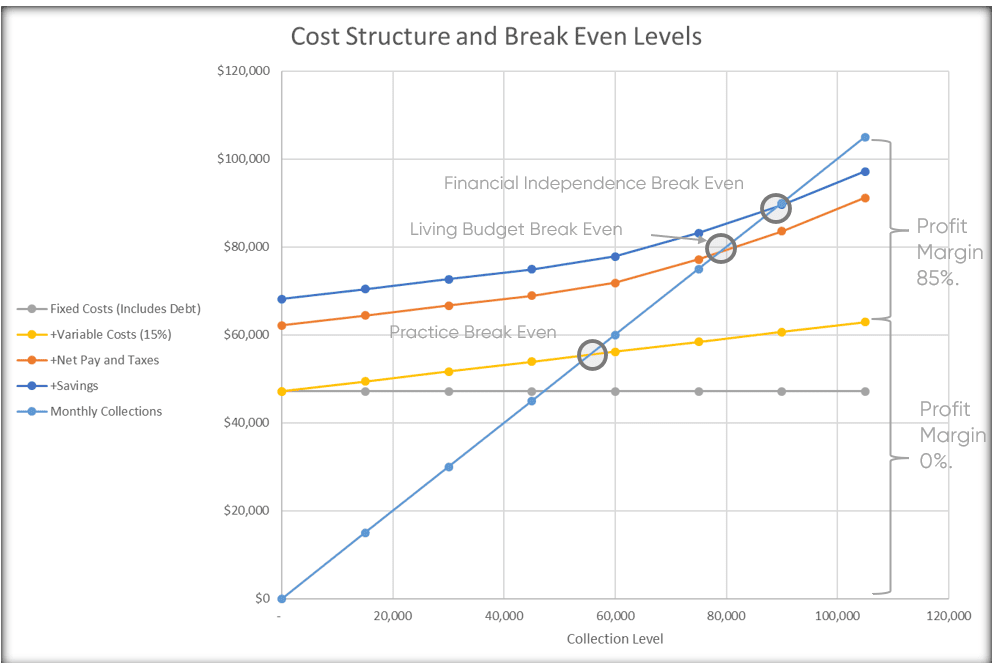

Alright, if you're on YouTube, please watch or jump on YouTube or I will try to narrate this. For those who are not on YouTube, let's dive into your breakeven. So what I'm looking at on the screen, it's a grid with a y axis and an X axis. And, uh, the x axis is the collection. So as we move horizontally from left to right, that's during the month, and this is a monthly view that I'm looking at.

You start off on day one. You open your doors, zero collections, first day of the month. Then as [00:05:00] you proceed throughout the month, you eventually get to the end of the month and you have a large, a larger amount of collections, obviously than day one. In my example, I'm showing on the screen we started zero and we end at about 120,000.

Now, if your practice is bigger, obviously that's gonna be a lot more than 120,000 potentially. Now on the Y axis are your financial obligations. That you have for the month. So let me, lemme start off with what I, what is the first financial obligation? These are what I call, or what, you know, in finance or economics, we call your fixed costs.

Your fixed costs. And they are costs that are, has the name states fixed, which means your pretty much are gonna pay these every month. Whether or not you have collections. Now, I want you to understand that it's not, this isn't a perfect explanation. It's not always gonna be completely black and white, what I'm about to tell you, but for the most part, it is true.

[00:06:00] Let's look at some of your fixed costs. A very easy, simple example of one of your fixed cost is rent. It doesn't matter whether you close down for the month, it doesn't matter whether you're open. 16 hours a day doesn't matter. You're gonna pay the same amount in your monthly rent. Now, if you own your building, you're gonna pay the same amount in the mortgage related to the acquisition of your building.

So that is a fixed. Cost doesn't change regardless of your collections. What else is fixed? I will say that your labor is fixed. Now granted, you may do some production based bonuses for your team, and I'm not talking necessarily about your associate, which may be a purely variable cost that you pay your associate a percent of collections.

That's that's not fixed. Most of your team is gonna be fixed, meaning that they're gonna show up in the morning, they're gonna leave at the end of the day, and regardless of the production, they're gonna be paid within some band of [00:07:00] consistency from month to month. Again, it's not perfect, but it is pretty much gonna be consistent from month to month.

Now, I, I know that in time it. Becomes a variable cost. If you double your collections, you're gonna have to hire a lot more and therefore your labor costs for your front office assistant and hygienes, et cetera, that's gonna go up over time. If you ex, if you sort of zoom out. From a one month period to, let's say a 10 year period, everything's gonna be ver a variable cost.

Everything's gonna be a variable cost. And by the way, I didn't mention this, beg this in the beginning, but there's just two primary types of costs that I'm focusing on here. There's fixed costs and there's variable costs. And so I'm starting off with the fixed costs and then I'm gonna get into variable cost.

But it's important that you know that this is in a finite period of time that I'm referencing when I decide what is fixed cost. And what is a variable cost, but in any business as that business doubles, triples, [00:08:00] quadruples. Revenue, everything becomes variable, even the rent, because you're gonna need more operatories.

And so you do a build out and you expand and you take on more rent, or you move into a bigger space, et cetera. Your employees, as you grow, you're gonna need more hygiene, you're gonna need more assistance, and that becomes a variable cost. Virtually everything becomes a variable cost in. Even like your phone bill, maybe you start to need more, more data or more lines or whatever that becomes a variable cost.

Everything is subject to change over time, but again, in this example, I'm really focusing on months to month. So during one month to the next, to the next, within, you know, a short period of time, what are, what's staying the same and what's a function during that month of your collection? So it goes up or down with your collections.

So back on fixed costs, your rent. Is one, your labor is one your, oftentimes your marketing is one. If you're paying a fixed marketing company, your [00:09:00] administrative costs are usually pretty fixed. What you pay for a bookkeeper, what you're paying in maybe certain ongoing legal fees, uh, or. Know, legal fees, actually, you're really not paying an attorney on a regular basis.

That's more transactional, but other fixed costs, um, on your p and l is your, the interest on your loan. So your debt, actually, if we, we look at your whole debt, we whole debt. Is a fixed cost. I mean, that's a classic example of a fixed cost. You play the same amount every month. Now, if you're on an interest only, then theoretically that's a variable cost, but that's not a variable attached to your collections.

That's a variable attached to the market rates of return, uh, what's called prime rate. That adjusts interest only debt up or down. But most of your debt is not gonna be interest only in your practice. And so that amount that you pay every month stays pretty much. Same. Now what are, therefore, I [00:10:00] think an easier way to look at this would would be to say virtually all of your costs in your dental practice are fixed except for two primary categories.

That's labor. I'm sorry. Sorry. That is labs and that is supplies, labs, and supplies. Those go up and down with collections for obvious reasons. Now, there's a few other things in there like. Collection or, or credit card processing fees. The more treatment you do, the more you collect, the more you're paying.

In Visa, MasterCard, discover processing fees, but that's a small item In terms of like kind of big nuggets on the p and l, it's your labs and supplies. Those are your primary variable costs from month to. So imagine a line in this example. I have all the fixed costs for the month equal about 40 on my screen.

It's looking to be about 45,000. In this example, if you're a bigger practice, obviously that's gonna be a bigger number. If you're a smaller practice, [00:11:00] that will be a smaller number, but 45,000 bucks and it's a straight horizontal line along this green. So even. At zero, we're at a hundred thousand dollars of collections.

It doesn't matter for that month. These are gonna be costs that you're pretty much gonna pay no matter what. And it's gonna be everything I just mentioned except for labs and supplies. So debt and then everything else. That's your first tier of fixed costs. Now I wanna step back and emphasize something about the unique nature of the economics of a dental practice.

A dental practice is intensely it, it's a, it's a. Intense fixed cost type of business because you buy all this equipment, you take on debt. The debt has a fixed cost. You're open a a consistent amount of time. You have teams that come in on a very fixed schedule. All of this creates this sort of consistent fixed cost structure.

There are some businesses that have a [00:12:00] smaller fixed cost, but a large variable costs. And the challenge with the fixed cost business, there's, there's both a challenge and a benefit. There's a pro and a con here with a business like a dental practice. The con is that if you have a bad month, you still have to pay all those fixed costs, which are about 80%.

Of your p and l. 'cause if you look at labs and supplies and talking about a general practice here, if you're a, say an oral surgeon and you don't have labs or pediatric dentist and you really don't have labs, then your, your variable costs are actually, actually less. But the, generally speaking, the fixed costs in a general dental practice are about 75 to 85% of.

Uh, of your cost structure is fixed and then you got about 20 to 25%. That's variable. And so the disadvantage here of the economics of a dental practice is that if you have some bad [00:13:00] months, because your fixed cost structure is such a large portion of your overall cost structure, your bank account balance can drop pretty quickly in order to meet those fi fixed cost obligations.

So if you have, if you're normally collecting, let's say a hundred thousand, and you go three straight months where you only collect 60,000, I guarantee you your cash is gonna drop pretty quickly because your overhead, your fixed costs aren't gonna go down very much. So if you're normally collecting the a hundred thousand and you only collected 60,000, you only collected 60% col of your collections.

You had a 40% decline, but I bet your fixed costs are pretty much the same. They may, may fall like 5% or so. And so if your fixed costs in that case are $70,000, you're gonna have to dip into your cash in order to cover not only your fixed costs, but then your variable costs and a few other outflows that I'm gonna talk about here in just a little bit.[00:14:00]

And up to this point of fixed costs, guess what your overhead is. I want you to, I want you to, that's a, that's a rhetorical question for now. I want you to think about that, and then near the end of the podcast, I'm gonna answer that question. But what is your overhead as a percent of revenue? It's a, it's a question we often ask ourselves as business owner, which is, what is my what?

What is my overhead percentage and what is my profit percentage? And my profit percentage is simply one minus my overhead percentage or a hundred percent minus my overhead percentage. So if my overhead percentage all in is 60%, then my profit percentage is 40%. And vice versa. If my overhead percentage is 40%, then my profit percentage is.

60% of revenue. They're sort of a teeter-totter to each other. And a lot of dentists will say, well, my overhead is X. My overhead is 55%, or my overhead is [00:15:00] 70% and my profit is 30%. You know, sometimes we use just these general, uh, big blocks to understand what is the profitability of our practice, and a general dental practice should be somewhere around 40% profitability.

Depending on where you live. In San Diego, it's a little bit less, it's close to about 37%. In other rural areas where cost of living is cheap, rent is cheap, that kind of thing, you might see a 45% profit margin for a dental practice, and then specialists, like an oral surgeon, is gonna be closer to 50%, sometimes 55%.

For oral surgeons, they just don't have a whole lot of overhead relative to the large revenue from their, their larger treatments that they do. Alright, so let num, let me now come back to this. And again, back on the screen. Is this grid and going from left to right horizontally, is this fixed cost structure?

It is a perfectly flat line. It doesn't decline and it doesn't incline. Now what's the next layer? Of [00:16:00] costs in your cost structure of your dental practice, it is variable costs. So in my example here, I'm gonna say that your variable costs are 15% of revenue, 15% of revenue. So as we go from from left to right, from zero collections on day one to 120,000 of collections at the end of the month.

This slope of variable costs. Therefore, it, it inclines throughout the month because the more you collect, the more you're paying for labs and the more you're paying for supplies. And now I know that there's a lag that you may be paying for labs and supplies, labs related to treatment that you did last month, or supplies that you're gonna use next month, but just.

Just generally speaking, as your collections go up, you're gonna be paying more labs and supplies, and so sitting on top of that fixed cost line [00:17:00] at about $45,000 or so on day one, your fixed cost and your variable costs start at the same point. They're at the same point, meaning that the variable cost layered on top of the fis, fixed cost is zero.

Is zero. You haven't paid any variable costs on day one. And then as you go throughout the month, that creates a spread, an incline above that fixed cost straight line then. Okay, so at this point, you've now covered your fixed costs, and now you've covered your variable costs. It would really help if you could watch this on YouTube to better understand or visualize what I'm displaying.

Now, in addition to paying your overhead, which is your, your fixed overhead is your labor, your facility costs, your marketing and your admin. Those are your, those are your and your debt. Those are your fixed costs. Then you layer around the variable costs of labs and supplies. Now, what's left? What's left?

Well, you have to pay yourself. [00:18:00] And you have to pay Uncle Sam. And so now there's this new line above the yellow line, which is the variable costs, that is amount of collections needed in order to pay your living expenses. So if you need $15,000 a month. To cover your personal living expenses and you're having to pay, let's say, $6,000 a month to cover all of your taxes.

That's fica. That's federal and state income tax. In order to cover all that, now you have a new line. Now, the interesting thing about this line, and this is gonna be the orange line, the interesting thing about this line is that now it's covering all your fixed costs. It's covering your variable costs of labs and supplies, and now it's covering your personal living expenses and your taxes.

Now this, this is great. One really interesting thing about this line is that it, as the month goes on and as you collect more, that orange line starts to steepen as it goes from left to right, starts to steepen, like you're starting to walk up a hill. And the reason why is as you make more money, every new [00:19:00] dollar of of income that you make.

Starts to get taxed at a higher rate. And that's the nature of a progressive tax scale. A progressive tax scale goes like this. Your first $15,000 of income, you don't pay anything in taxes, nothing. Your next $20,000 of income, you only pay at 10%. Now, making these numbers up a little bit, but if you actually Google the tax code, uh, the federal tax code, you'll see these steps and what the rate is at each step.

So now we're up to $30,000. The next $40,000 might be taxed at 25%, and then as you keep going, eventually the highest federal bracket is at 37%. 37%. And if you're married filing joint, you hit that at around 600,000 or so. If you're single, you hit that somewhere around $300,000 or so, and now every new dollar.

After you hit that amount is taxed at that higher [00:20:00] bracket. So if every month you're starting to collect more, then as you collect more, you have to budget for a little bit more taxes per unit of dollar made. Now, if you have a good CPA, a good financial consultant, you can really try to erode the taxes and bring, bring that back in your pocket through different strategies.

That's what we do a ton here at Practice. CFO Wealth accumulation is much more greased, I will say, if we can reduce that massive friction of taxes. So this, that's a big thing as we help our doctors become financially independent as financial planners, is to help them on the tax side, and that's why financial planning for a dentist, in my opinion, needs to be done by somebody who truly understands the cash flows inside of the dental practice.

Because that advisor can give really good tax advice. 'cause most of the tax reduction is gonna occur on the inside of your dental corporation, not on the outside, in your personal account. [00:21:00] And good financial planning is also gonna encompass good tax planning, which means we got to look at the cash flows in the business to really do that.

Right? Alright, so now if you can collect enough to meet your fixed costs, your variable costs, and. Your net paid yourself and your taxes. Now you're able to live. You're living, you're enjoying your life. Today. Everything is covered except for one thing. At this point. Everything's covered. Your overhead, your debt, your taxes, your living expense, they're all covered except for one thing.

What do you think that is? I'm gonna tell you. It is your future self, IE setting aside money every month in savings, setting aside money on your personal balance sheet, your personal net worth statement that will be used to grow, accumulate, and then eventually spin off income that will take care of you.

And so the last line on my display, on my visual here is a blue line that includes an amount of your [00:22:00] collections going towards savings. Now, so I've got four lines. I got your fixed costs, which include debt. I've got your variable costs of labs and supplies. I've got your net pay and taxes for your lifestyle and taxes, and then I have savings for your future self.

That is the universe of everything that you need to cover, and that's a lot. Now, if I draw a diagonal line from the. Very bottom left corner of this grid where it's zero, and again, the Y axis going up and down. That's the, that's the cost of these various inflection points, these various breakevens, these various costs within your cost structure, both business and personal.

That's what's going up. So you start at zero and at the very top of the screen, I have $120,000. Your overhead, your fixed overhead is about 45. Your variable costs go up over time. They're 15% of your collections. Your taxes and pay is another [00:23:00] roughly 20,000 or so, 22,000, and then I have savings on here for about another seven or 8,000.

In this example, what those numbers are in actuality related to you is gonna be a function of your own practice overhead, your own tax situation, your own personal budget needs, and your own future goals and savings. So. The numbers I'm using clearly just an example here, and then again the, the x axis on the bottom from left to right, that's your collections.

So imagine now this, I have this, this light blue line that goes from zero on the very bottom left and it sort of curves exactly evenly splitting this grid, uh, by going from left to right and top or bottom to top. So it just basically moves forward at a 45 degree angle, like a steep straight hill. And this assumes that every day you're just kind of collecting a consistent amount throughout the month.

And by the end of the month, let's [00:24:00] say in my example here, I'm showing about $105,000. At that point, you have pierced each one of these breakevens in order to satisfy those and make progress financially. Now, on this graph, there are three key points. Number one. These are the three breakevens that I refer to.

The first one is your practice breakeven. This is what I call, this is this totally west made up terms, but I use it here a lot at practice CFO. It is your practice breakeven, and this is the amount of collections you need in the month in order to cover your fixed and your variable costs. So your labor lab supplies, facility marketing and admin, and your debt, all of that, that is your practice break even.

Meaning that if you stopped at that point of collecting just enough to take care of those things, you can keep your doors open. Great. You're not [00:25:00] going under, you're not gonna file bankruptcy. That said, you haven't paid yourself anything. You might as well go work an In-N-Out burger 'cause you're gonna make more money.

Ultimately taking home into your personal account. If you're only collecting your practice enough to cover your fixed and variable costs, you're not taking anything home to you, let alone even paying some taxes. At that point, you actually aren't gonna own any taxes because pretty much all of your costs are gonna be tax deductible, not all of it.

The principle on your debt repayment to the bank is not tax deductible, but, but your. For the most part, not gonna pay a whole lot of taxes if you're only collecting enough to cover, to cover your labor lab, fac, uh, your labor labs, um, supplies, facility marketing and admin, and your debt, because your net income on your profit loss statement is gonna be zero.

We're pretty close to it. And if your net income is zero, you're not gonna pay taxes, assuming that you didn't also issue yourself a large W2. But bottom line is there's really no operating income and therefore there's no [00:26:00] taxes to pay if you don't have a net income. And worse, if you're at a loss, well, you're definitely not gonna pay taxes if your company is running a loss.

Alright, so that is what I, what I call my practice a breakeven. Let's go on to the next breakeven. I have three breakevens. The second one is your living budget breakeven and your living budget breakeven is that amount of collections you need in order to cover your fixed costs, variable costs, and debt.

Now also to cover your living expenses and your taxes. That's called your living budget break even because it's covering everything, including your living budget and your taxes. Now, in my example on this screen, it's right at about $80,000 of collections that you have met all your fixed costs, you met your taxes, and you have enough to pay yourself that amount of roughly 15,000 per month to live on.

Now, the first breakeven, the practice breakeven was right at around $57,000 or so. If you collected 57 in the month, now you've covered [00:27:00] your labor lab supplies, facility marketing and admin, and your debt. Then you keep going and you get to $80,000 in collections. Now you're covering paying yourself and paying the tax agencies.

That was one more break even, and this is the break even that covers all those fixed cost, variable cost debt covers your lifestyle expenses today and your taxes. Then it covers also the funding of your personal balance sheet to take care of you later. This is what I call your financial independence break even.

And if you're a client of practice CFO, every month we issue you the CFO analysis report. And one of the pages is what is your financial independence break even? What do you need to collect in order to pay for your overhead debt, taxes, et cetera? And. Yourself and also now to fund your retirement goals.

That is financial independence breakeven. I personally don't like the [00:28:00] word retirement or retirement planning. I like the word financial independence or financial freedom, the concept of financial independence. Is there a point in time when you are no longer depending on working in order to take care of yourself?

Financial independence. If you could literally watch Netflix all day every day, and you and your, all of your living expenses are covered, that is financial independence. Who wants to do that, but you know what I mean. Whether that's golfing all the time, traveling the world, spending a lot of time with kids or grandkids donating money to your church or doing church service, whatever that is that you want to do, that doesn't earn income.

And once you have enough assets to fund your ability to do that, so you don't have to work, that is being independent, financially speaking. So that is our financial independence breakeven or what I, in short form call fi breakeven. That's where we want to go. And in this graph I'm looking at right now, it's right at about $90,000, $90,000.

You [00:29:00] cover everything. Now, in this example, if you were to able to keep going and eke out more, let's say you collect a hundred thousand dollars, well now you have an extra surplus and I love it. When I meet with the client, we sit down, we're looking at the financials. I've already pre prepped a, a financial forecast.

I've already defined what I believe is the surplus. It's a beautiful conversation when there's surplus after I've already sort of budgeted our tax payments. We've already planned for your overhead costs. I know you're covering your debt, your personal living expenses. We're funding some money now into our retirement.

Let's say you're funding 10,000 a month into your 401k plan or defined benefit plan or IRAs. Once all that's done, I love it when I see even extra. Because then we're, we get to have just that fun conversation of, Hey, what do we wanna do with this? Do we wanna pay down any debt? Do we want to invest in growing your practice by building out another operatory?

Usually I prefer just taking out a loan for that [00:30:00] kind of thing, 'cause it's pretty low rate and tax deductible. But do we wanna fund it into a brokerage account and go invest in a, in a prudent savvy investment allocation in the stock market or the bond market? Do you want to go buy a rental property and save it up for that?

Do you wanna put it into your kids' 5 29 education savings account? Do we need to build up an emergency reserve so you feel really comfortable with the amount in your business and personal checking accounts at all time so you don't lose sleep over insufficient cash? What is it that we want to do with this?

And those are just some of the best parts of financial planning is when you get there. So the way that I look at this is when I meet with a doctor, the first order of business is to try to make sure we have enough collections to at least for now, meet our living budget break even. And in some cases, if your practice isn't quite there or you're a newer practice owner and you have a lot more debt from buying the practice, or maybe a lot more student loans, maybe live in a more high cost area, we have to try to keep your personal budget [00:31:00] down.

Because at the end of the day, if you're having financial struggles, it's either because you are not earning enough or your expenses are too high, one or the other. And so the way to fix it is you get your collections up. In the practice or your, your, your, your income up. Maybe you work a day or two a week as an associate somewhere outside of your practice in order to supplement your income.

And that's very common if you're starting up especially, or you gotta go cut your expenses either in the practice or, and or in your personal life. It's one of those two things. Now, the strategies can get a lot more involved when you start looking at budgeting, tax planning, cashflow planning, debt structuring.

There's various things you can do from a structural or a strategy, strategy standpoint in order to create the cashflow needed. But sometimes it's just the, it's just the hard truth. You gotta go spend less, period, and sometimes it's a combination of the strategy and the financial discipline as well.

Alright. Now let me answer the [00:32:00] question I posed earlier on in the podcast. What is your overhead percentage? Somebody asks you what's your overhead, overhead percentage? I'm gonna tell you your overhead percentage or your profit, I will say, which is the inverse of your overhead, your profit, what's left effort over overhead.

Your profit up to the point of paying your fixed and variable costs is zero because every single dollar and a hundred percent of that dollar. Goes to paying your labor lab supplies, facility marketing and admin, and your debt, a hundred percent of that does. And so your profit margin is zero. So if you ended off the month with $55,000 in collections, in this example, your profit margin was zero.

Now, from after that though, after you've met your labor lab supplies, facility, marketing and admin, and your debt, once you've covered those costs in your collections during the month. Let's say you're on the 18th of the month and you have collected [00:33:00] $58,000. In my example, this very first circle, that practice break, even at that point.

At that point you have now covered all of your overhead and your profit up to that point was 0%, but now guess what? Any collections above. Your fixed and variable costs, any collections above that amount has virtually yes, any dollar above that amount ends up going 85% to you because every new dollar that you collect, every new dollar that you collect is only gonna pay for the new variable costs, the new labs and the new supplies on that new dollar of collections.

And so that's why this becomes a really more granular way of answering that question is what is your profit margin? Now? Yes, at the end of the month with when all is said and done, you'll blend these two and you'll say, my profit margin was 42%. But I just want you to under understand [00:34:00] conceptually that as you progress through the month.

Your profit margin is zero until you pierce your fixed costs and after your fixed costs, your profit margin ends up being 85% because you're only spending about 15% for labs and supplies. This is why that extra case, that extra day of being open, that extra treatment plan presented being accepted, that extra little bit that you eek out there near the end of the month makes the world of difference.

It makes the world of D difference because that's where you get the majority of your profit is in those extra cases, and then you're really, you're really dropping money to your bottom line. And that's, that's critical. So what I would do is I'd look at your finances, at your financial statements and kind of understand, you can do a little analysis or work with your CPA and ask them the question, what is my fixed cost, [00:35:00] which includes my debt?

What is that amount? Is that 40,000? Is it a hundred thousand? Do you have a large practice and your fixed cost is 200,000? What is that amount? And you can park that in your head and the more you think about it, it's like you're doing a. Intuitive way of measuring. And when we measure things, it's like we're keeping our eye on it.

And when we do that, it motivates behavior to go a little bit more and to perform a little bit better. It's like measuring your diet and if you're trying to lose weight or measuring your speed and running a 10 K or a marathon, when you measure it, it gives you something to benchmark against in order to take your next step of effort to progress more and do better next time.

So if I run your numbers and I say, Hey doctor, you're overhead. Your fixed costs, they're really about, they're really about 70,000 and we know based on your labs and your, maybe you have a CAD cam and so you're only maybe 10% for labs and supplies. Now we're starting to get a really good idea of at what point during the month when you're collecting do you hit that [00:36:00] practice breakeven, and now everything after that goes toward your living budget and your financial independence.

Okay, this is, this episode is on breakevens cost structure and breakeven levels, and the takeaway from this one is to get your finances. Ask your CPA, what are my fixed costs? What are my variable costs, and what do I need to collect in order to meet all of those obligations and then meet my taxes and my spending?

And then what is my additional amount needed if I wanna set aside $10,000 a month? Now that's gonna be a little bit of an analysis for the CPA to do. If you go with a model more like a practice C-F-O-A-C-F-O or a finance model, this is sort of very inherent to the type of analysis, uh, we do at the company in order to give that education to our clients, to then make really good decisions and to ideally motivate them, motivate them to get to that level, to not just get.

To the living budget break even, but really get past that into the [00:37:00] financial independence break even. Alright everybody, I hope you found this one helpful. In the next episode, we are gonna go into completing a tax plan, and I do think this will be really valuable to tax plan because a lot of dentists, and I won't say a lot.

Just people in general, business owners don't quite understand what tax planning is in their head. It's, you get some tax deductions. There's a tax strategy, there's some of sort of a silver, silver bullet or a cure all tax planning strategy and some really complicated attorneys will come and present things which are.

In so many cases, just a horrible idea that leaves that is very expensive and leaves the bag held by the doctor in the event of an audit where it's 99% sure gonna fail. These things happen a lot. When I'm at the California Dental Association, I see a number of these types of companies just selling [00:38:00] product, these legal products that are just dangerous, and I've seen them.

Flop many times and really cost the doctor a lot of money and a lot of times. So I'm gonna talk to you about what is healthy, good, effective tax planning as a dental practice owner. So stay tuned for that. Until next time, have a great one.

Wes knows what's best for dental practices. He's been doing this for a long time and he sees lots of practices. He can tell me how our practice is doing, and what we can do to increase our productivity. With past CPA's, there were no ideas. It was all coming from me, saying "I think I can do better, but I don't know how." I come in to meet with Wes and he says "You CAN do better, and I know how."

PracticeCFO is in hundreds of dental offices around the country. They know what numbers should look like. They know what percentages of payroll, rent and supplies should be, and they will hold you accountable to those numbers, which will really help you stick to your plan and your path of growth and savings. That is invaluable

Whenever something comes up, whether it's building or practice related and we weren't sure where the numbers would go, PracticeCFO has been instrumental in helping us figure that out. I can't say enough of how important that is - that it goes beyond that initial partnership. They make sure this business marriage works.

When I go home from work, I don't spend a whole lot of time stressing about what my books look like, or how much I owe in taxes. By using PracticeCFO, the burden of keeping track of a lot of the big financial numbers and metrics are taken off my plate.

PracticeCFO helped me develop a plan for the future. I have colleagues that work with other accountants that don't have a plan - they just look at the numbers of the practice and that's it. There's no plan for 10, 20 years from now. But with PracticeCFO, you get that. PracticeCFO makes you feel like you're they're only client.

(In reference to his practice sale) What could've been super stressful, wasn't! When picking John and Wes, it was from word of mouth recommendations and other people's experiences from the past that really did it for me. And it turns out that those recommendations were right on the line.

Wes knows the business side of dentistry. His comprehensive plan will organize your personal and professional finances so you can focus on taking care of patients. Massive ROI.

I can’t say enough good things about everyone at PracticeCFO. Everyone on the team is professional, organized, knowledgeable, helpful and kind. They also respond to emails and phone calls immediately and are always happy to help. They have helped me navigate year-to-year as a business owner. PracticeCFO gives me peace of mind that my business is in good hands.

I love Practice CFO! They have helped me obtain a practice and maintain a practice. They are incredible people who are on top of everything and make owning and running the business portion of a practice easy. They couldn’t be better for my business and my sanity. They have every detail of the business and taxes taken care of where all I have to do is show up and follow their easy steps to success!

Practice CFO has the best tools I’ve seen for personal tax and financial planning in addition to top-tier corporate tax and accounting services. I have been very pleased with the level of quality service. They manage my monthly bookkeeping and accounts payable. It is a great system and saves me a ton of time, and it allows us to have monthly financial statements within a week of month end.

This will close in 0 seconds

{kind=link}